.png)

Automate your family office

Schedule DemoHeading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

TL;DR:

This wealth management checklist covers 13 essential areas for single family offices. Use it to set up a new office or optimize existing operations, and track progress in Asora by assigning owners, linking documents, and reviewing consolidated dashboards weekly. Then, revisit quarterly to maintain momentum.

A Practical Framework for Family Office Ops

Setting up or running a single family office feels like building a plane while flying it. You need governance documents, entity structures, data feeds, performance calculations, reporting schedules, compliance controls, and operational workflows to streamline the client onboarding journey. All while managing actual investments and serving stakeholders who expect answers immediately.

Most wealth management professionals learn this through trial and error. Investment and financial advisors working with high-net-worth individuals often lack experience with the operational complexities family offices face. The wealth management playbook for advisory onboarding is well established, and many of those principles adapt cleanly to families building in-house operations.

This wealth management checklist provides a comprehensive framework that encompasses governance, data management, reporting, and controls. No fluff. No theory. Just the must-haves that make the wealth management business run smoothly while improving client satisfaction and establishing trust.

Who This Checklist Is For & How to Use It

This wealth management checklist serves single family offices with lean teams (2-20 people) managing 5-50 entities. If you're a wealth manager at a multi-family office or financial advisor at an RIA, parts will be relevant, but some items assume you're managing for one family rather than acquiring more clients across different households.

This covers operational infrastructure, not investment strategy, tax advice, or legal counsel. You still need your tax professional for tax planning and to provide tax guidance, an estate planning attorney for trusts and living wills, and an investment advisor for portfolio construction.

Specialized advisors assist with a wide range of financial planning topics, including health savings accounts, retirement goals, savings and investment strategies, tax-efficient planning, healthcare funding, and long-term income management.

This checklist focuses on the operational backbone that enables everything else to function correctly.

How to use it: Work through sections weekly. Assign owners to each item, including those with client signatures, and mark those that require approval. Mark what you have, what needs work, and what's not applicable. Revisit quarterly as your financial situation evolves and circumstances change.

You don't need to download anything or fill out forms. Use this as your reference and adapt it to your specific needs. This organized approach ensures that nothing falls through the cracks, creating a consistent experience across reporting cycles.

13 Must-Haves for Family Office Success

Running a family office is more than managing money; it is about building a structure that protects, grows, and governs wealth across generations. With a strong foundation, operations stay smooth, data remains reliable, and decisions are made with clarity. The following 13 must-haves outline the practical essentials that keep a family office efficient, compliant, and ready to scale.

1. Strategy & Governance

Start with clarity about why the family office exists and how decisions get made. This creates the foundation for establishing trust with both family members and external advisors.

Document the family's long-term financial goals. Is this about wealth preservation for future generations? Capital appreciation to fund philanthropic ambitions? Supporting the family business? Your mission drives everything else, including your wealth management strategy. Consider how philanthropy and a giving strategy fit into your broader objectives.

Your investment policy statement (IPS) translates the mission into specific allocation targets, risk limits, concentration guidelines, and rebalancing triggers. It's the constitution for investment decisions:

- Document risk tolerance explicitly so investment decisions align with comfort levels.

- Include liquidity policy (minimum cash buffers, emergency fund targets, capital call reserves) and co-investment rules (thresholds, approval requirements, concentration limits).

- Consider tax-loss harvesting opportunities and whether investments should be structured to be tax-deductible or tax-free where possible.

A clear RACI (Responsible, Accountable, Consulted, Informed) makes it easier for everyone to see how decisions get made and who’s involved at each step. Approvals for investments, valuations, and wires should have named owners so that authority isn’t left to guesswork. Once that structure is written down, the team can move faster and avoid confusion.

It also helps to separate what requires board input, what the CFO can handle, and what falls under the officers' purview. Defining these routes for activities such as new investments, rebalancing, and manager changes ensures consistent and transparent decision-making.

Regular meetings give the work rhythm. Monthly operations reviews, quarterly investment committees, and an annual strategy session give space for reflection and planning. With agendas in place and decisions captured in minutes, the team has a reliable record of what was agreed and why.

Where Asora helps: Store your mission statement, IPS, liquidity policy, and governance documents in the documents vault linked to relevant entities and assets (wherever applicable) so they're accessible when making decisions.

2. Structure & Entities

Understand and document your organizational structure. This clarity prevents confusion for the client during the onboarding journey for new family members and advisors.

- Current org chart: Map ownership across all entities. Who owns what percentage of which trust, holding company, or SPV? This becomes your entity map showing the whole structure.

- Look-through to SPVs and trusts: Many families hold investments through multiple entity layers. Document look-through ownership showing ultimate owners, not just immediate legal title.

- Legal names, jurisdictions, registrations, signatories: Maintain an entity register with full legal names, formation jurisdictions, tax registrations (EIN, VAT numbers), and authorized signatories for each entity. This supports the onboarding process when opening new accounts or working with new clients (service providers).

- Bank and broker relationships: Document which banks and brokers serve each entity. Record mandate limits, signing authorities, and sweep arrangements.

- Change log: Track when entities are created, restructured, or retired. This matters for tax reporting and future reference when questions arise about historical structure.

Where Asora helps: Asora’s Wealth Map visualizes ownership across trusts and SPVs with look-through capabilities. The platform maintains entity registers with detailed legal information and tracks bank and broker relationships for clients, including linked mandates and limits.

3. Client Onboarding & KYC (People, Accounts, Managers)

Proper onboarding creates the foundation for everything else. A strong client onboarding process fosters a professional relationship from the outset.

People

For all beneficial owners and authorised signatories, have a complete KYC pack on file: photo ID, proof of address, source-of-funds/source-of-wealth documentation, and sanctions/PEP checks. This underpins compliance and builds credibility with banks and other counterparties.

Beneficiary details should be up to date across pensions or retirement plans, life assurance policies, and any assets that name beneficiaries. A quick review of disability cover ensures the family has adequate protection if income stops.

At the initial meeting, set clear expectations for the necessary documents, their submission requirements, and the submission deadline. Use a simple checklist and a secure upload method so the admin is painless and trackable.

Custodian and Brokers

Each account should be opened with complete and verified documentation, ensuring a smooth setup process through internal reviews and external checks. Data feeds that automatically pull position and transaction details save time and reduce the likelihood of manual errors. Access rights also need to be clearly defined, indicating who can view which accounts and who has the authority to act.

Third-Party Managers

For external investment managers and funds, complete due diligence questionnaires (DDQs), document fee structures, define reporting specifications (including report types, frequency, and format), and establish service-level agreements (SLAs) for response times and data delivery.

This onboarding experience sets the tone for the ongoing relationship.

Where Asora helps: Store all onboarding documents in the vault, organized by entity, person, or manager. This improves the onboarding experience for both you and your service providers.

4. Data Aggregation

Clean, timely data is the foundation of good wealth management and client satisfaction.

- Custodian and broker feeds: Connect to all custodians and brokers via automated data feeds. This automatically updates positions, transactions, market values, and corporate actions.

- Private asset data capture: For investments without custodian feeds (such as private equity, venture capital, real estate, and direct investments), establish standardized templates for capturing commitments, calls, distributions, valuations, and fees.

- Cash and loan accounts: Don't forget operating accounts, savings accounts, credit lines, and margin loans. Track cash needs across all entities so you maintain adequate liquidity buffers and emergency funds.

- Naming conventions: Establish consistent naming for accounts, entities, and holdings. This prevents the same entity from being referred to by three different names in different reports, thereby improving the client experience.

- Instrument mapping: Map securities across different custodians to a single master record. One custodian might reference Apple by ticker AAPL, another by CUSIP, another by ISIN. Map these to one position.

- FX sources: Document the source of foreign exchange rates and the time at which they are obtained. This matters for consistency and audit purposes, particularly when calculating capital gains.

- Daily and weekly reconciliation: Set up processes to reconcile custodian feed data against monthly statements. Flag exceptions for investigation to manage risk and maintain data quality.

- Data SLA: Define how current your data should be. Close-of-business for liquid accounts? Quarterly NAV plus roll-forwards for private assets? Document this so everyone has aligned expectations.

- Documents: Link supporting documents to each holding: account statements, capital account reports, fund financials, appraisals, and loan agreements.

Where Asora helps: Set up data feeds to banks and custodians. Asora guarantees a connection to any bank that offers data feed connections, thereby eliminating the need for manual statement downloads during the client's onboarding process.

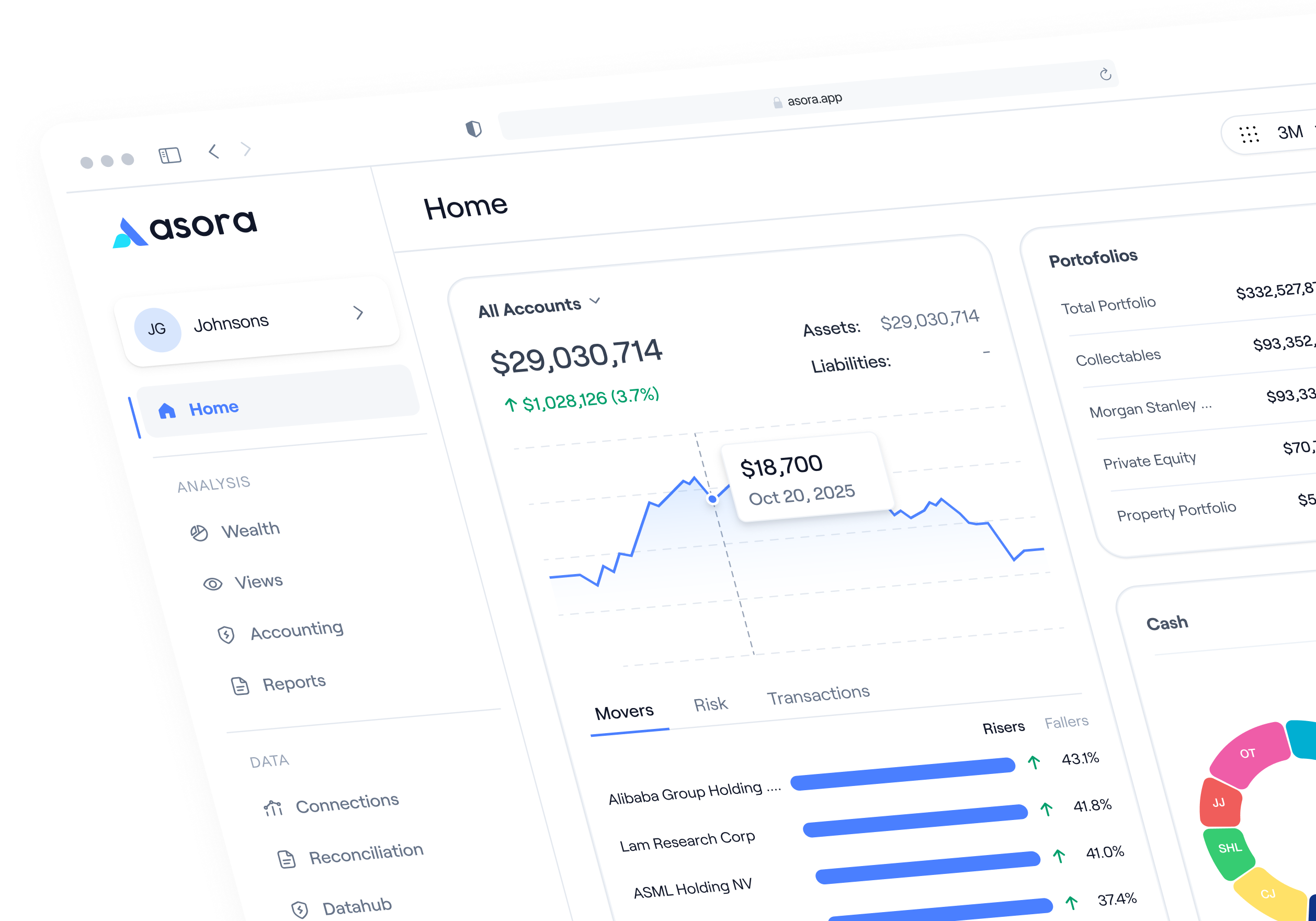

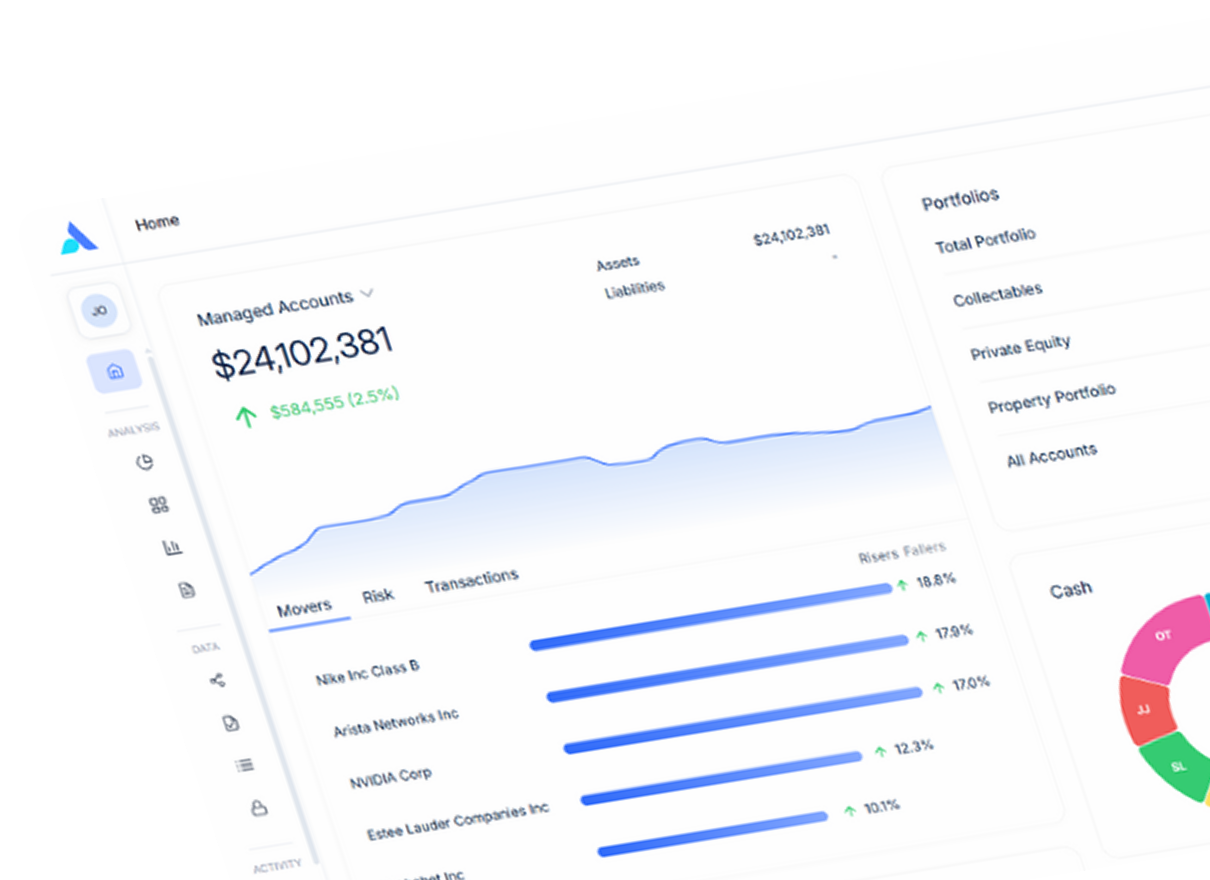

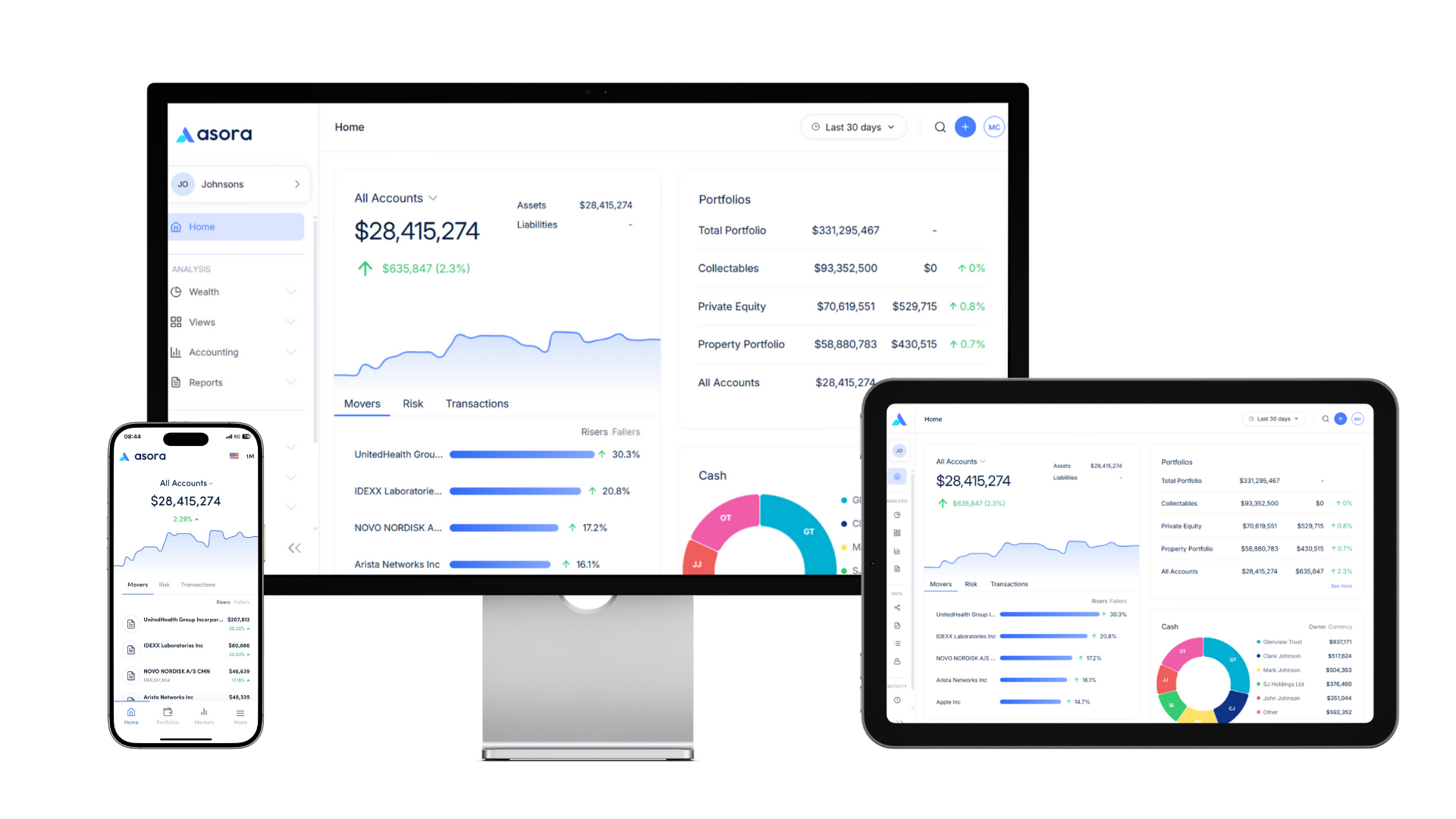

5. Portfolio & Performance

Performance measurement requires a transparent methodology and consistent application across your investment portfolio.

- Benchmarks: Define appropriate benchmarks for each asset class and strategy. Public equities may be benchmarked against the S&P 500 or the MSCI World. Private equity to Cambridge Associates or Burgiss indices. Real estate to NCREIF or similar.

- Policy weights and drift bands: Document target allocation percentages and acceptable drift ranges. If the target is 30% public equities with a ±5% band, rebalancing triggers at 25% or 35% of the target. This helps mitigate risk systematically.

- Performance methods: Use the time-weighted return (TWR) for liquid portfolios when evaluating manager skill independently of cash flows. Use the internal rate of return (IRR) for private investments where cash flows are both timing- and magnitude-sensitive. Consider unitization for beneficiaries sharing pooled investment vehicles. Utilize both methodologies to gain a comprehensive understanding of performance.

- Close calendar: Establish month-end and quarter-end close schedules. Define cut-off times for transaction inclusion. Document variance analysis procedures comparing actual performance to benchmarks and expectations.

- Restatement policy: Define when and how you'll restate prior period performance. Restating should be rare and require documented justification, rather than being a routine practice.

Where Asora helps: Performance monitoring calculates benchmarking, IRR, Multiple, and TWR using appropriate methodologies for different asset types. The platform handles the complexity of performance calculation, allowing you to focus on analyzing results rather than building spreadsheets.

6. Private Assets (PE/VC/RE/Credit/Other)

Private investments require more manual attention than custodian-held securities in your portfolio.

- Holdings register fields: For each private holding, capture vehicle name, strategy type, vintage year, investment stage, total commitment, funded amount, remaining commitment, management fees, performance fees, and preferred return terms.

- Capital account roll-forward: Between quarterly NAV reports from fund managers, maintain roll-forwards showing opening NAV, capital calls, distributions, estimated appreciation, and ending NAV. This keeps the report current, even when official fund reports lag.

- Unfunded commitments: Track what capital remains callable. This is an obligation that affects your actual liquidity position and informs future investment pacing.

- Distribution waterfalls: Document how distributions flow, including preferred returns, catch-up provisions, and carried interest splits. This helps you model future distribution scenarios and evaluate investments appropriately.

- Valuation policy by asset type: Define how each type of private asset gets valued and how frequently. Quarterly NAV from funds? Annual appraisals for real estate? Mark-to-market for publicly traded but illiquid securities?

- Fair-value adjustments: Document process for when you disagree with manager-reported valuations or need to adjust between formal valuation dates. Require approval notes explaining the rationale.

- Debt and loan schedules: For investments involving leverage, track loan balances, interest rates, maturity dates, covenants, and collateral pledged.

Where Asora helps: Private assets are centralized, with complete registers capturing all relevant fields. The platform tracks commitments, capital calls, distributions, and valuations in one place, and uses custom fields and workflows to document valuation decisions and debt terms

7. Reporting

Different stakeholders require different perspectives on the same underlying data. Quality reporting enhances client satisfaction and can lead to increased referrals from satisfied clients.

- Stakeholder map: List everyone who receives reports: principals, family members, board members, lenders requiring covenant compliance reporting, tax advisors needing specific data cuts (including required minimum distributions), estate planning attorneys reviewing trust portfolios, and insurance coverage summaries for risk management.

- Report types: Define standard report formats. Entity-level reporting maintains a legal structure for tax purposes. Consolidated reporting rolls up to family totals. Look-through reporting shows ultimate beneficial ownership. Beneficiary unitized views show proportional interests in pooled vehicles.

- Cadences and cut-offs: Establish reporting schedules. Monthly flash reports by day 5 of the following month? Quarterly comprehensive packs by day 10? Annual reports by January 20? Document cut-off dates for transaction inclusion.

- Commentary template: Standardize what narrative accompanies numbers, such as Executive summary, performance analysis, changes versus the last period bridge, manager updates, tax foundation for decisions, etc.

- Version control and archive: Implement version numbering for all reports. Archive historical versions with timestamps that show who produced what and when.

- Distribution permissions: Define who can access which reports. Some family members see everything, others see only their specific trust, and external advisors see only what's relevant to their scope.

Where Asora helps: The platform drives multiple reporting views from a single ownership structure. It allows users to generate customizable exportable reports tailored to the needs of different stakeholders. You can create templates for each audience and produce consistent reports from the same underlying data, ensuring more stakeholders receive timely information.

8. Cash, Liquidity & Treasury

Managing liquidity effectively requires forward visibility and clear, well-defined processes. Utilizing sweep accounts and optimizing cash deployment enhances returns while maintaining safety.

- 90-day cash ladder: Project cash inflows and outflows for the next 90 days. Include expected distributions, planned capital calls, tax payments, operating expenses, and planned investments.

- FX plan: If you have exposure to multiple currencies, document your approach to foreign exchange. Natural hedge versus active hedging? Spot conversions versus forward contracts?

- Credit lines and covenants: Track available credit facilities, current utilization, interest rates, and financial covenants (debt-to-equity ratios, minimum net worth, concentration limits). Monitor covenant compliance every month to mitigate risk.

- Capital call calendar: Maintain a forward calendar of expected capital calls based on fund commitments, typical pacing for each strategy, and vintage year.

- Funding playbooks: Document procedures for meeting capital calls, including which accounts are tapped first, what triggers selling securities versus using credit lines, who approves each funding source, etc.

- Sweep rules: Define how excess cash is deployed, whether via automatic sweeps to high-yield savings, investment sweeps to money market funds, or manual deployment, while optimising and maintaining sufficient emergency liquidity.

- Sign-offs for large transfers: Establish thresholds requiring additional approval. For example, transfers exceeding $100,000 require CFO approval, and transfers over $1M require principal sign-off. Clear delegation creates accountability.

- Dual control: Implement maker-checker controls for wire transfers. One person initiates, another approves.

Where Asora helps: The Liquidity dashboard gives a consolidated view of cash by entity, bank, and currency, so teams can quickly see what’s available and where it sits. You can filter and group balances, add context by linking documents to the relevant assets or entities, and keep evidence one click from the numbers, while approvals and transfers continue in your external banking process

9. Operations, Tasks & Approvals

Operational discipline prevents things from slipping through cracks and improves the onboarding experience for new team members.

- Monthly close checklist: Document every step required to close the month. Reconcile custodian feeds. Update private asset valuations. Accrue fees. Calculate performance. Run reports. Review with stakeholders. Archive final versions. Assign owners and due dates for each step.

- Quarter-end and year-end extensions: Quarterly and annual closes typically require additional steps, including more comprehensive reporting, external audit support, preparation of tax packages (with capital gains calculations), and board presentations. Document these extended procedures with prepared agendas.

- Recurring tasks: Beyond monthly close, maintain lists of recurring operational tasks. Reconciliations (daily/weekly), fee accruals (monthly), private asset valuations (quarterly), regulatory filings (annual), insurance renewals (annual), and KYC refreshes (every 2-3 years).

- Maker–checker approvals: Define which activities require dual control to ensure accuracy and accountability, including valuation adjustments, manager changes, and significant rebalancing; document approval paths that show who can approve what, along with the appropriate client signatures.

- Escalation paths: Define what happens when a normal approver is unavailable, name a backup approver, and set a timeline before escalating further.

- SLA tracking: Monitor whether you are meeting internal service levels, confirm reports are delivered on time, and ensure exceptions are cleared within target timeframes.

Where Asora helps: Workflow functionality supports task management and deal pipeline tracking. The platform can assign tasks, set due dates, and track completion.

10. Security & Compliance

Protecting sensitive family data isn't optional for wealth management clients with significant assets.

- SSO/MFA: Implement single sign-on where possible and enforce multi-factor authentication for all users. Passwords alone aren't sufficient protection for individuals with substantial portfolios.

- Least-privilege permissions: Grant access based on what each user needs for their role. Principals see everything. Staff see what they work on. External advisors see only relevant portions. Review permissions quarterly as roles evolve and life changes occur.

- Joiner/mover/leaver procedures: Document how you handle changes to user access and account management. New hires get provisioned with appropriate access during their onboarding checklist. Role changes trigger permission reviews. Departures trigger immediate access revocation. This protects you and your clients.

- Audit logs: Maintain records of data access and changes required for compliance, capturing who viewed which records and when, and who modified which values, to create accountability and support investigations if questions arise.

Data residency and encryption: Specify where your data physically resides and how it is protected, with encryption in transit and encryption at rest as standard for wealth-management clients. - Vendor security documentation: Collect security certifications and documentation from all service providers handling sensitive data, such as SOC 2 reports, ISO 27001 certification, and penetration-test results, and work only with vendors that demonstrate strong security practices.

- Data Processing Agreements (DPAs): For vendors processing the personal data of EU residents, ensure proper DPAs are in place that satisfy GDPR requirements.

- Incident response plan: Document actions for a security breach or data loss, specifying who is notified, the communication plan, and the steps to contain and remediate, so client relationships are protected even during crises.

- Backups: Maintain regular backups of critical data. Test restoration procedures annually to ensure backups actually work when needed.

Where Asora helps: The platform enforces MFA with granular user permissioning. Data is encrypted in transit and at rest. Asora maintains ISO 27001 certification and GDPR compliance, providing the security infrastructure that wealth management clients expect.

11. Documents & Knowledge

Information is only helpful if you can find it when you need it.

- Taxonomy and naming: Establish consistent folder structures and file naming conventions to ensure clear organization and identification, whether by entity, asset type, document type, or other criteria. Pick a system and stick with it.

- Versioning: Implement version control for documents that change over time. Annual appraisals create new versions. Amended and restated operating agreements supersede prior versions. Make it clear which version is current for reference.

- Retention policy: Define retention periods for each document type, for example, permanent retention for governing documents such as living wills and powers of attorney (as set by estate-planning attorneys), seven years for tax records, and one year for monthly account statements if quarterly statements are retained.

- Link documents to holdings and transactions; don't just store them in folders. Connect them to what they document. Link LP agreements to the specific fund investment. Link appraisals to the property they value. Link the capital account statements to the private equity position.

- Search standards: Ensure documents are searchable. This means OCR for scanned PDFs and consistent metadata tagging. Staff should be able to quickly find the necessary paperwork.

- Board portal versus investor share rooms: Define access boundaries by specifying what information belongs in the governance-accessible board portal and what is shared in investor-specific folders.

Where Asora helps: Documents link directly to relevant assets, entities, and transactions. The platform supports tags for flexible organization. External providers (such as fund managers, appraisers, and accountants) can upload documents via secure external links directly to your instance, streamlining client onboarding and ongoing operations while reducing staff burden.

12. Accounting & GL Coordination (If Applicable)

If you maintain a general ledger for accounting, coordinate it with your wealth management system to ensure accurate financial records.

- Chart of accounts alignment: Ensure your portfolio management classifications map logically to GL account codes. Public equities might map to specific GL accounts, while private investments might map to others.

- Sub-ledger to GL mapping: Define how investment data flows to your accounting system. Is the wealth platform a sub-ledger feeding GL? Or are they parallel systems reconciled every month?

- Accruals for fees and tax: Your accounting system should accrue management fees, performance fees, and tax liabilities between payment dates. Coordinate timing between portfolio and accounting systems.

- Intercompany eliminations: For consolidated financial statements across multiple entities, document intercompany transactions and elimination procedures.

- Audit requests: Maintain a standard checklist of typical audit requests, covering investment details, fee calculations, and performance attribution, so supporting documentation can be provided quickly.

- Export granularity and controls testing: Define what data exports to accounting systems and in what format.

Where Asora helps: The platform lets you view dividend receipts, monitor withholding tax rates, and track manager fees, bank charges, and custodian expenses. Custodian holdings are reconciled automatically, with mismatches flagged for review. This supports your accounting process even though Asora isn't a GL replacement.

13. KPIs & Continuous Improvement

Measure operational performance to improve over time. This systematic approach builds advantages that compound and can lead to more referrals from satisfied stakeholders.

- Data quality KPIs: Track metrics that indicate data health, including the percentage of positions with current valuations, the average age of private-asset NAVs, the percentage of holdings with linked supporting documents, and the share of reconciliation exceptions cleared within 48 hours, so you know where to focus improvement efforts.

- Reporting KPIs: Monitor the effectiveness of reporting by measuring the percentage of reports delivered on time, the average time from month-end to delivery, the number of restatements required, and the rate at which review comments are resolved before final distribution.

- Quarterly retrospective: After each quarter-end close, run a brief retrospective that captures what went well, what caused delays, what errors occurred, and what should change next quarter, so the team learns and avoids repeat issues.

- Policy change log: Document when policies get updated and why. This creates institutional knowledge about why things work the way they do, preventing the need to revisit old debates. Keep this for reference when circumstances change.

Where Asora helps: Workflow tracking provides data for measuring cycle times. Policy documents stored in the vault can document the evolution over time.

How to Put It to Work in 30 Days

This might feel overwhelming. Here's a light plan for new clients or existing offices wanting to improve:

Week 1: Governance, entity register, data map

- Draft or review your investment policy statement covering financial goals and risk tolerance

- Document current entity structure and ownership

- Map all accounts, custodians, and data sources

- Assign owners to each area of this onboarding checklist

- Schedule initial meetings with key stakeholders for setting expectations

Week 2: Feeds live, naming standards, reconciliation queue

- Connect data feeds to major custodians using digital platforms where available

- Establish naming conventions for accounts and holdings

- Set up initial reconciliation procedures

- Begin linking documents to holdings for reference

- Implement the right onboarding software if manual processes are overwhelming

Week 3: First close run, private asset roll-forwards

- Execute the first month-end close using the new procedures

- Build private asset registers with current positions

- Create capital account roll-forwards for PE/VC holdings

- Test performance calculations on sample data, including capital gains

- Review insurance and disability policy adequacy

Week 4: Stakeholder reports, approvals, archive

- Generate initial reporting packs for different stakeholders

- Implement approval workflows for key decisions with appropriate signatures

- Archive reports with proper version control

- Conduct retrospective: what worked, what needs improvement

- Celebrate progress and plan next quarter's improvements

This provides you with an operational foundation in just one month. Then iterate and improve quarterly as conditions change and you fully leverage your systems.

Bringing It All Together

This wealth management checklist outlines the operational backbone that enables family offices to function effectively.

Clarity prevents confusion. Controls prevent errors. Cadence creates predictability.

Together, they produce speed (faster decisions), trust (reliable information), and audit-readiness (defensible documentation). This foundation supports a range of services, including financial planning, retirement savings optimization, charitable strategies, and estate planning coordination.

You don't need to implement everything perfectly before you start. Work through sections systematically, assign owners, establish rhythms, and improve incrementally. The families that do this build advantages that compound over time.

Whether you're establishing a new family office or improving an existing operation, this onboarding checklist provides the framework. Use it to coordinate with wealth advisors, portfolio managers, financial advisors, and your tax team to take full advantage of the operational discipline that drives success. The personal touch comes from adapting these principles to your specific situation while maintaining the operational discipline that creates success.

See how Asora helps operationalize this checklist with our all-in-one wealth management platform. Request a demo to explore how your structure could work in Asora.

FAQ

Q. What should be included in a wealth management checklist?

A family office checklist should cover governance, structure, onboarding, data aggregation, performance, private assets, reporting, liquidity, operations, security, documentation, accounting, and KPIs for ongoing improvement. Asora supports these areas with aggregation, performance, documents, and workflows in one system.

Q. How do you create a wealth management onboarding checklist?

Cover the full client onboarding process for all stakeholders:

- Collect IDs and proof of address for beneficial owners during the initial meeting

- Document source of funds and conduct sanctions/PEP checks

- Review coverage and disability insurance adequacy

- Gather beneficiary designations for accounts, life policies, and open custodian and broker accounts

- Establish data feed connections using onboarding software for automated position updates (Asora connects to banks and custodians and centralises documents)

- Complete due diligence on external managers, including DDQs and fee documentation (store and link in Asora for easy reference)

Q. What are the most important areas for family office operations?

Data aggregation, performance measurement, and reporting are critical. Connect to custodians and track private assets for complete visibility, calculate TWR for liquid holdings and IRR for private investments, and produce consistent reports. Asora delivers these with consolidated views across entities and linked evidence.

Q. What technology helps implement a wealth management checklist?

Your technology should handle multiple areas simultaneously:

- Data aggregation to connect to custodians and banks

- Portfolio management to calculate performance and track private assets

- Document management to link evidence to holdings

- Workflow tools to assign tasks and track approvals

- Reporting to generate stakeholder-specific packs from consolidated data

Look for integrated solutions, such as Asora, that cover these checklist areas on a single platform, so you don't need separate tools for each function.